You’re sitting on your couch, scrolling through your phone, and you decide to check the zillow value of my home just for kicks. Suddenly, your heart jumps. Maybe the number is $50,000 higher than you thought. Or, more likely, it’s dropped $20k since last Tuesday and now you’re wondering if the local real estate market is cratering.

Stop. Take a breath.

The Zestimate is basically the weather app of the housing world. It gives you a general idea of whether you need a jacket, but it shouldn’t be the reason you decide to sell your parka and move to Florida. Most homeowners treat that digital number like gospel. It isn't. It’s an algorithm, and algorithms don't have eyes. They’ve never seen your brand-new quartz countertops or smelled the weird dampness in your basement that only happens after a heavy rain.

How the Zestimate Actually Works (and Where it Trips Up)

Zillow is pretty open about how they calculate the zillow value of my home. They use a neural network-based model that sifts through millions of data points. We’re talking about public records, tax assessments, and user-submitted data. In 2022, they even started incorporating "spatial" data, which means the algorithm tries to understand how your house relates to the ones next door.

But here is the kicker.

Zillow itself admits that the Zestimate has a median error rate of about 2.4% for on-market homes. That sounds small, right? On a $500,000 house, that is $12,000. For off-market homes—the ones most of us are just casually tracking—that error rate jumps significantly. In some rural areas, the margin of error can be over 7%. If you are relying on that number to plan your retirement or your next move, you are basically gambling with a huge chunk of your net worth.

The algorithm loves "comparables." If three houses on your street sold for $400,000 recently, Zillow is going to peg your house around $400,000. It doesn't care that your neighbor’s house was a "fixer-upper" with 1970s shag carpet and your house is a fully renovated mid-century modern masterpiece. To the computer, you're both just a three-bedroom, two-bath ranch on a quarter-acre lot.

The Problem With Public Records

Public records are often late. Sometimes months late. When a house sells, the deed has to be recorded with the county, then digitized, then scraped by Zillow’s bots. If the market is moving fast—like it did during the 2021-2022 frenzy—the zillow value of my home might be reflecting data that is already three months old. In a shifting market, three months is an eternity.

There is also the "junk in, junk out" problem. If the tax assessor’s office has your home listed as having 1,800 square feet, but you added a permitted 400-square-foot sunroom five years ago, Zillow won't know unless you manually update your home profile. Most people don't.

Why Your Neighbors Influence Your Value More Than You Think

Have you ever noticed your Zestimate change because a house three blocks away sold? It’s annoying. You didn't change anything, yet your "wealth" just fluctuated. This happens because of "proximity weighting."

If a house nearby sells for a low price due to a divorce or a fast foreclosure, it drags down the "neighborhood average." Zillow sees a sale at $320,000 and assumes the area is cooling off. It doesn't know that the seller was desperate or that the house had a foundation issue. Conversely, a "bidding war" sale can artificially inflate your zillow value of my home to a level that no appraiser would actually support.

Honestly, the Zestimate is a starting point. It's a conversation starter. It is definitely not a professional appraisal.

Does Zillow Want to Be Wrong?

Not really. They actually spent years (and millions of dollars) on a Kaggle competition to improve their algorithm. They want to be the "source of truth" for real estate because that’s how they sell leads to real estate agents. But real estate is local. Intensely local. A house on the left side of a busy road might be worth 15% less than a house on the right side because of the school district boundary. Algorithms struggle with those invisible lines.

How to Make the Zillow Value of My Home More Accurate

You actually have some control here. You don't have to just sit there and take whatever number the bot gives you.

- Claim your home. If you haven't "claimed" your home on Zillow, do it. It allows you to verify the facts.

- Correct the specs. Check the bedroom count, bathroom count, and square footage. If they are wrong, the Zestimate is guaranteed to be wrong.

- List your upgrades. Did you put on a new roof? High-efficiency HVAC? Zillow has a section where you can check off these features. It won't instantly add $20,000 to your value, but it helps the model refine its estimate over time.

- Check the "Home Report." This shows you exactly which "comps" Zillow is using to value your house. If you see a house on that list that is a total dump, you can sometimes flag it as "not a comparable" to help clean up the data.

It’s worth noting that Zillow isn't the only player. Redfin has its own estimate. Realtor.com has one. Chase Bank even has one for mortgage holders. If you really want to know what your house is worth, look at all four. If Zillow says $450k and Redfin says $410k, the truth is probably somewhere in the middle.

The Human Factor: What Machines Miss

I once saw a house that had a Zestimate of $600,000. It looked great on paper. But when you stood in the backyard, you realized it was directly underneath a high-voltage power line that buzzed. No algorithm is going to pick up on the "buzzing" sound that makes a buyer walk away.

Similarly, the zillow value of my home can't account for "curb appeal." A house with a beautifully landscaped yard and a fresh coat of modern paint will always sell faster and for more money than a beige box with dead grass, even if the square footage is identical.

Market Sentiment vs. Data

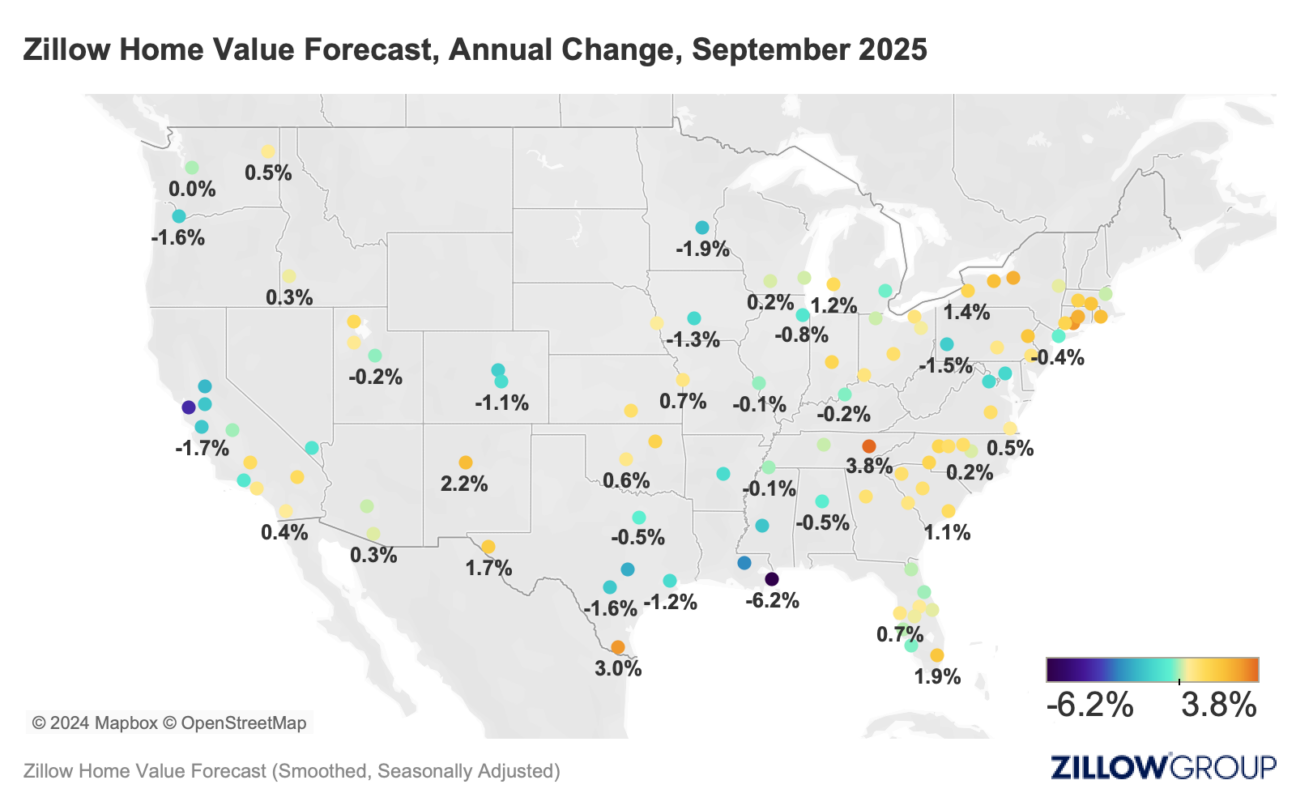

In late 2025, we saw a lot of "stale" inventory. Homes were sitting for 60 days instead of 6. When this happens, Zestimates tend to stay high while the "real" market price is dropping. This is because the algorithm needs "sold" data to update. It can't sense the "vibe" of a market where buyers have suddenly stopped showing up to open houses.

Actionable Steps to Determine Your Real Home Value

If you are actually planning to sell, or if you are looking to do a cash-out refinance, stop staring at the Zestimate. Here is how you get a real number.

1. Get a Comparative Market Analysis (CMA). Any decent local real estate agent will do this for free. They look at the "active," "pending," and "sold" listings. Crucially, they look at the pendings. These are houses that have a contract but haven't closed yet. This is the most current data available, and Zillow usually doesn't have the final sale price of a pending home until it officially closes.

2. Look at Price Per Square Foot (With Caution). Calculate the average price per square foot of the last three sales in your immediate neighborhood. Multiply that by your square footage. It’s a blunt instrument, but it’s a good reality check against a wild Zestimate.

3. Account for "The Big Three." Roof, HVAC, and Foundation. If yours are old, subtract $10,000 to $15,000 from whatever the zillow value of my home tells you. Buyers will find these during an inspection, and they will want a credit.

4. Hire a Professional Appraiser. If you want the absolute truth for a legal reason (like a divorce or estate planning), pay the $500–$700 for a licensed appraiser. They are the only ones whose opinion actually matters to a bank.

5. Track the Days on Market (DOM). Look at Zillow’s "Days on Market" for your area. If the average is 10 days, the Zestimate is probably conservative. If the average is 50 days, the Zestimate is likely overinflated.

The bottom line? The zillow value of my home is a tool, not a conclusion. Use it to track trends over years, not to make financial decisions over days. Treat it like a ballpark figure. If it says your house is worth $500k, assume it’s actually worth somewhere between $475k and $525k. That $50,000 swing is the "reality gap" where life, negotiations, and human emotion actually happen.

Start by verifying your home's data on the platform to ensure the baseline is at least accurate. Then, cross-reference that number with at least two other valuation sites like Redfin or your bank's internal estimator. If you see a discrepancy of more than 5%, it's time to call a local professional who can provide a "boots on the ground" assessment of your property's true competitive position in today's specific local climate.