If you’ve been watching the tickers lately, you know the vibe around Zeta Global is... complicated. Honestly, it’s a bit of a rollercoaster. Just when you think the "AI marketing" narrative is finally setting into a steady groove, the market throws a wrench in the gears.

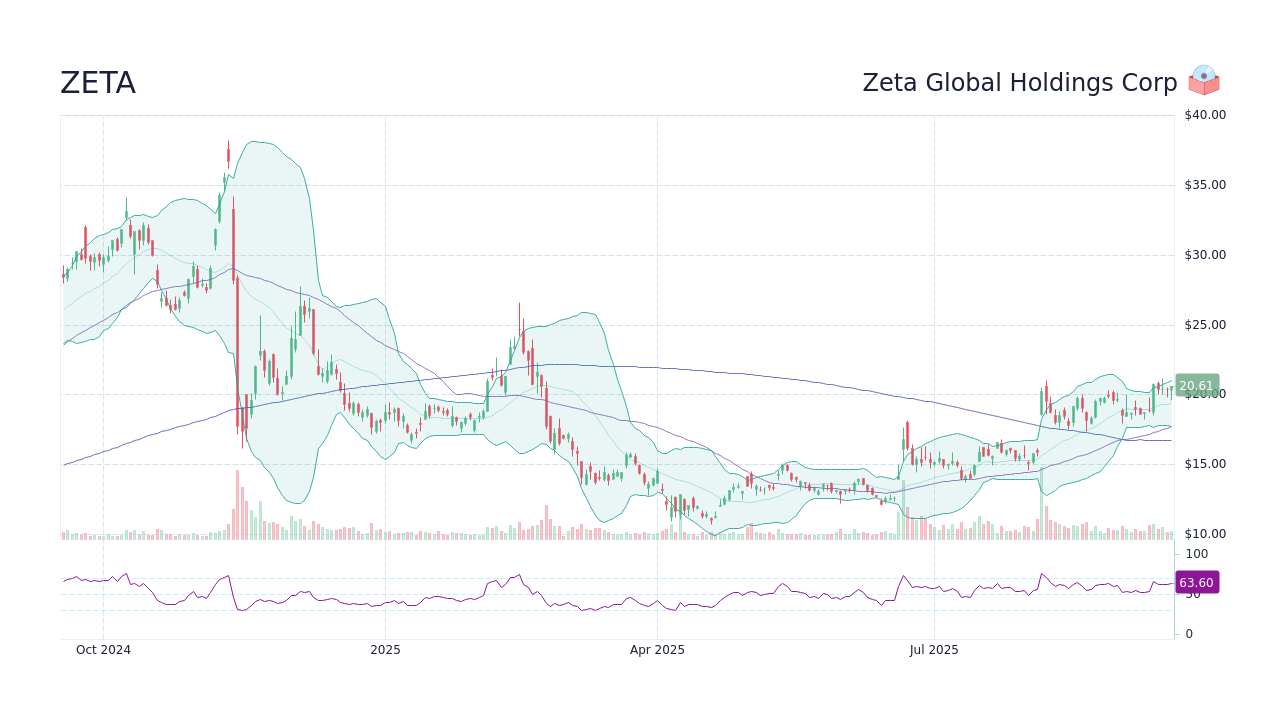

Zeta stock price today took a noticeable breather, closing at $20.26 on Friday, January 16, 2026. That’s a roughly 6.1% slide from the previous day.

Why the sudden dip? Well, markets are twitchy. Part of it seems to be tied to a family trust filing to sell about 262,000 shares—which, in the grand scheme of a $5 billion company, isn't a massive structural shift, but it’s enough to make day traders hit the sell button. Plus, the broader tech sector is feeling some heat right now. When the big guys like Nvidia get bruised by global trade news, the "mid-cap" AI names like Zeta usually feel the sting twice as hard.

The Reality Behind the $20 Mark

It’s easy to look at a one-day drop and panic. But if you zoom out a bit, the story changes. Just a week ago, Zeta was pushing closer to $24. In fact, it hit a 52-week high of $26.60 not that long ago.

We’re seeing a classic tug-of-war here. On one side, you have the bulls who are obsessed with the "beat and raise" streak. Zeta has basically become the overachiever of the MarTech world, consistently topping revenue estimates for 17 quarters in a row. That’s not a fluke; it’s a pattern.

But on the other side? The bears are still whispering about the 2024 short-seller report from Culper Research. Even though David Steinberg (the CEO) and his team came out swinging with rebuttals and a massive buyback program, some investors still have "short-seller PTSD." They see any downward movement as a sign that the "other shoe" is dropping.

Personally, I think the "consent farm" allegations and the noise about their data collection have mostly been priced in by now. The company is literally under the hood of 450+ enterprise clients who aren't exactly known for doing sloppy due diligence.

Breaking Down the 2026 Outlook

What actually matters for the Zeta stock price today isn't just today's closing number—it's where the floor is.

- Initial 2026 Guidance: Management is projecting $1.54 billion in revenue.

- The OpenAI Factor: They just doubled down on their partnership with OpenAI at CES 2026. They're integrating "agentic" AI into their Athena platform. Basically, instead of just sending emails, the AI acts like a digital consultant for brands.

- Profitability Hurdles: They still aren't GAAP profitable. For a lot of old-school investors, that’s a dealbreaker. They're generating free cash flow ($209 million projected for 2026), but the net income is still in the red due to heavy stock-based compensation.

Why the Market is Acting So Weird

You've probably noticed that Zeta doesn't move like a normal stock. It moves in "chunks."

When DA Davidson or Citi reiterates a "Buy" rating (which they both recently did with price targets in the $26–$29 range), the stock jumps 10%. When a single insider sells a tiny fraction of their holdings for "tax planning" or "estate management," it drops 5%.

This volatility is the price of admission for mid-cap AI. Zeta isn't a "safe" utility stock. It’s a high-growth engine that’s trying to prove it belongs in the same conversation as Salesforce or HubSpot.

The Institutional Grip

Interestingly, institutional ownership is sitting around 87%. Big funds like Greenvale Capital and Norges Bank have been increasing their stakes. When the "smart money" is buying the dips while retail investors are panic-selling on Reddit, it usually tells you that the long-term thesis is still intact.

The company also has about $199 million left in its stock repurchase program. That’s a massive safety net. If the price falls too far, the company itself steps in to buy back its own shares, which helps stabilize the floor.

Actionable Next Steps for Investors

If you're holding ZETA or thinking about jumping in, don't just stare at the 1-minute candle.

Watch the February 24th Earnings Call. This is the big one. This is where they’ll confirm if the OpenAI integration is actually driving new "super-scaled" customers (the ones paying $1M+ a year).

Check the Sector Momentum. Zeta is currently tethered to the "AI Application" trade. If software stocks are up, Zeta flies. If there’s a "rotation" back into value or energy, Zeta gets left behind.

Mind the Gap. There’s a technical gap on the chart around the $18.50 level from late last year. In a worst-case scenario where the market continues to slide, that’s the area where buyers likely step in with force.

Buying Zeta stock price today at $20.26 might feel like catching a falling knife, but for those who believe in the "agentic AI" shift, it’s looking more like a discounted entry into a company that’s growing 20%+ year-over-year while most of its peers are stalling.

Pay attention to the free cash flow margins. As long as those keep expanding toward that 14% target, the short-term price swings are mostly just noise in a much louder growth story.