The financial press is currently sleepwalking through a narrative of "market drift." They look at the recent extension of the Iran ceasefire and see a non-event. They see a cooling of tensions. They see a geopolitical "nothingburger" that allows investors to get back to the serious business of tracking the Fed’s next sneeze.

They are dead wrong.

What the consensus calls "market focus drifting elsewhere" is actually a collective failure to price in the structural decay of the petrodollar and the intentional weaponization of uncertainty. This isn't a ceasefire. It is a strategic pause designed to recalibrate the cost of regional dominance. When the media tells you the market has "moved on," what they really mean is that the market has stopped looking at the fuse while the bomb is still ticking.

The Myth of the Geopolitical Discount

For decades, traders have operated on the "Goldilocks" theory of Middle Eastern tension: enough friction to keep oil prices profitable for producers, but not enough to actually break the global supply chain. This extension is being read as a continuation of that status quo.

I’ve spent years watching desks ignore the secondary effects of these "diplomatic wins." When a ceasefire is extended not out of a shared desire for peace, but because both sides are running low on conventional leverage, you aren't seeing stability. You’re seeing a pressure cooker with a taped-down valve.

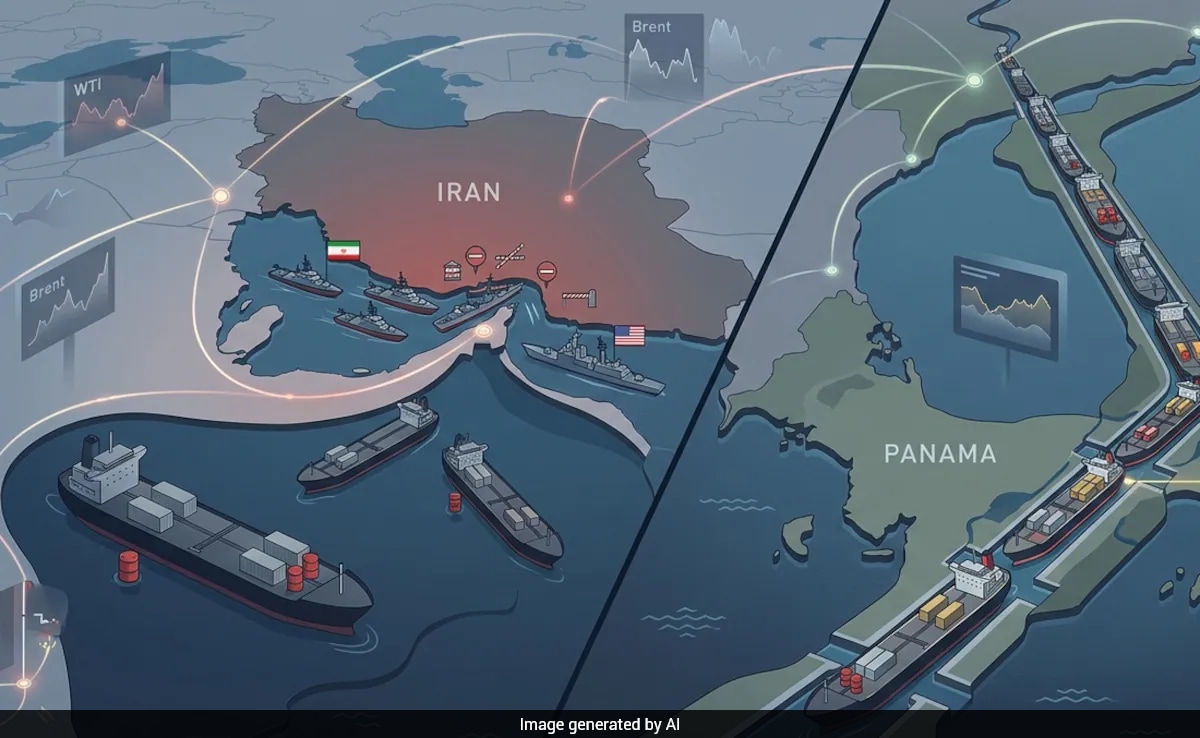

The "drift" the competitor article mentions is actually a dangerous complacency. The premium on Brent crude should be reflecting a massive risk of transit disruption in the Strait of Hormuz, yet it sits flat. Why? Because the market believes the executive pen is mightier than the ballistic missile.

The False Narrative of "Stability Through Extension"

Let’s dismantle the premise that an extension equals a reduction in risk. In the world of high-stakes diplomacy, an extension is often a tactical withdrawal to facilitate a more surgical strike later.

- Inventory Management: Iran isn't using this time to find religion; they are using it to harden their nuclear infrastructure and diversify their shadow fleet.

- Currency Hedging: The real story isn't the ceasefire—it’s the accelerating rate at which Tehran is settling energy contracts in non-USD currencies.

- Political Theatre: For the Trump administration, this isn't about peace. It’s about optics for the domestic energy sector. By keeping the lid on a full-blown conflict, they prevent a gas price spike that would incinerate political capital.

If you are managing a portfolio and you think the "Iran problem" is solved because of a signature on a page, you have fundamentally misunderstood how leverage works. You are treating a temporary truce as a structural shift. That is a mistake that costs billions when the "drift" inevitably snaps back to reality.

Why the "People Also Ask" Crowd is Wrong

The typical retail investor asks: "Will the Iran ceasefire lower gas prices?"

This is the wrong question. The right question is: "How does this extension accelerate the formation of a BRICS-led energy bloc?"

The "drift" in market focus is exactly what the architects of this shift want. While everyone is looking at tech earnings or the latest retail sales data, the actual plumbing of the global energy market is being rerouted. Russia, Iran, and China are not spectators in this "ceasefire." They are the beneficiaries of the US's attempt to manage a multi-polar world with a uni-polar toolkit.

By extending the ceasefire, the US maintains a facade of control. But under the hood, the trust in the US Treasury as a neutral arbiter of global trade is eroding. Sanctions have lost their bite because the targets have built their own playground.

The Fallacy of the "Priced-In" Risk

You’ll hear analysts on CNBC claim that "Middle East risk is priced in." This is a lie told by people who need to fill airtime. You cannot price in a black swan that is actively disguised as a white swan.

A truly "priced-in" risk would show up in the volatility surface of oil options. Instead, we see a skew that suggests traders are betting on a perpetual sideways grind. They are selling vol because they think the ceasefire extension provides a floor.

Imagine a scenario where a single drone strike—deniable, unattributable, and perfectly timed—hits a major processing facility in Abqaiq. The "drift" vanishes in seconds. The market, currently positioned for "nothing to see here," would face a liquidity vacuum.

I saw this in 2019. I saw it again during the initial waves of the Red Sea disruptions. The market forgets the lessons of kinetic reality the moment a diplomat smiles for a photo op.

Stop Looking for Peace; Start Looking for Friction

The most contrarian move right now is to stop believing in the "de-escalation" narrative. Friction is the new global constant. The ceasefire is merely a change in the frequency of that friction.

Instead of following the "drift," look at the following:

- Insurance Premiums for Maritime Freight: While the "market" ignores Iran, Lloyd’s of London isn't. Follow the money in risk mitigation, not the noise in the headlines.

- Gold and Hard Asset Accumulation: Central banks in the East are buying gold at a clip that suggests they don't believe the "ceasefire" era will last.

- Refinery Utilization Rates: Watch where the physical barrels are actually going. The paper market is a casino; the physical market is a courtroom.

The competitor's piece argues that the market has "moved on." This is the same logic used by people who walked through the surf right before the tsunami hit because the water had receded. The "drift" is the recession of the water.

The Petrodollar’s Long Goodbye

The true underlying mechanism here is the decoupling of energy from the Dollar. Every time there is a "crisis" followed by a "ceasefire" that involves Iran, we see more bilateral trade agreements that bypass the SWIFT system.

The ceasefire extension is a sedative for the Western investor. It keeps the "drift" going while the structural transition happens in the dark. We are moving toward a world where a US President's extension of a ceasefire matters less than a Chinese President's guarantee of a purchase order.

If you are waiting for a clear signal to hedge, you’ve already missed the window. The signal is the very quietness you see now. The lack of movement is the warning.

The Actionable Reality

Forget the "drift." Forget the "focus elsewhere."

If you are long global equities without a significant tail-risk hedge in the energy sector, you are gambling on the continued patience of a region that has run out of it. The ceasefire isn't a bridge to a better future; it’s a pier. You can walk to the end of it, but eventually, there’s nowhere to go but down.

The "drift" is a collective hallucination. The extension is a stay of execution. The smart money isn't looking elsewhere—it's quietly exiting the room before the door locks.

Buy the volatility while it’s cheap. Because when the "focus" returns to Iran, the price of entry will be ruinous.